A crypto-backed loan lets you borrow cash or stablecoins against your digital assets without selling them. For a long-term holder, that is the appeal: you unlock liquidity, keep your upside, and avoid triggering a taxable sale — one of the few situations where taking on debt can be a smart financial move. The catch is that your collateral can be sold out from under you. Everything that follows — how much you can borrow, and how easily you get liquidated — comes down to one number: the loan-to-value ratio.

How Crypto Loans Work

You pledge crypto as collateral and receive a loan worth a fraction of it. Because crypto is volatile, lenders never let you borrow the full value; they demand a buffer, and they watch that buffer in real time. If the collateral falls too far, the lender sells part or all of it to repay the loan. There is no phone call, no negotiation, and on a 24/7 market it can happen at 3 a.m. while you sleep.

This is the same mechanism whether you borrow through a company (CeFi) or a smart contract (DeFi). What differs is who holds your keys, how the trigger is calculated, and how forgiving the process is. Understanding the ratio behind it is the whole game.

In practice a loan runs through a simple lifecycle:

- Deposit crypto as collateral and choose your loan size — that sets your opening LTV.

- Receive the loan in cash or stablecoins, typically without selling and without a taxable event.

- Interest accrues while the loan is open; you monitor your LTV (or health factor) as prices move.

- Repay any time — most lenders charge no prepayment penalty — to unlock your collateral, or add collateral if your LTV climbs.

- If your LTV hits the liquidation threshold, the lender sells collateral automatically to bring the loan back in line.

What Your LTV Really Means

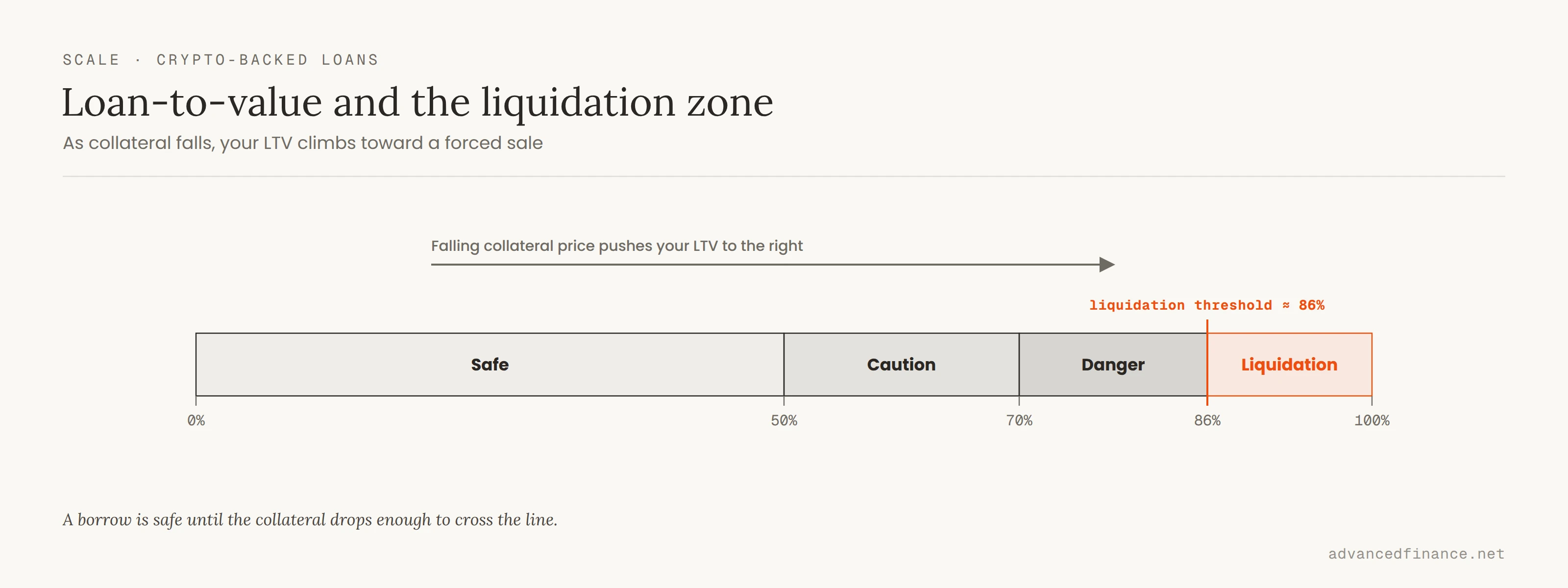

The loan-to-value ratio is your loan divided by the market value of your collateral. Post $60,000 of Bitcoin and borrow $30,000, and your LTV is 50%. As the collateral price moves, that ratio moves with it: if Bitcoin drops, the same loan becomes a larger percentage of a smaller collateral value, and your LTV climbs toward the danger zone.

There are really two numbers that matter. The opening LTV is the most you can borrow at the start — commonly around 50% on volatile collateral. The liquidation LTV (sometimes called the maintenance margin or liquidation threshold) is the level at which the lender starts selling. On Coinbase's onchain loans, for example, that threshold sits around 86%. The gap between the two is your cushion, and closing it is what liquidation feels like from the inside.

DeFi protocols express the same idea as a "health factor." On Aave, health factor = (collateral value × liquidation threshold) ÷ debt. Ten thousand dollars of ETH at an 80% threshold backing a $6,000 loan gives a health factor of (10,000 × 0.80) ÷ 6,000 = 1.33. When that number falls below 1, liquidation begins (Aave documents the exact health-factor and liquidation mechanics). It is the same math as an LTV limit, written upside down.

How Liquidation Is Triggered

Here is the part most guides skip: your liquidation price is not where you bought, and it is not where you opened the loan. It is fixed by your loan size and the platform's liquidation LTV — nothing else.

Suppose you post 1 BTC and borrow $40,000 on a platform that liquidates at an 86% LTV. Liquidation triggers when your debt reaches 86% of your collateral's value — that is, when 1 BTC × price × 0.86 = $40,000, or a Bitcoin price of about $46,500. It does not matter whether you opened that loan with Bitcoin at $60,000 or at $100,000: the liquidation price is the same $46,500, because it depends only on the loan and the threshold.

This is why loan size is the real lever. Borrow half as much — $20,000 against the same 1 BTC — and the trigger drops to roughly $23,300. You have doubled the distance the market must fall before you are liquidated, using nothing but restraint. On most platforms the liquidation itself is also partial before it is total: Aave, for instance, closes up to half the debt while the position is only mildly underwater and moves to a full liquidation once the health factor falls far enough. Either way, you crystallize a loss at the worst possible moment.

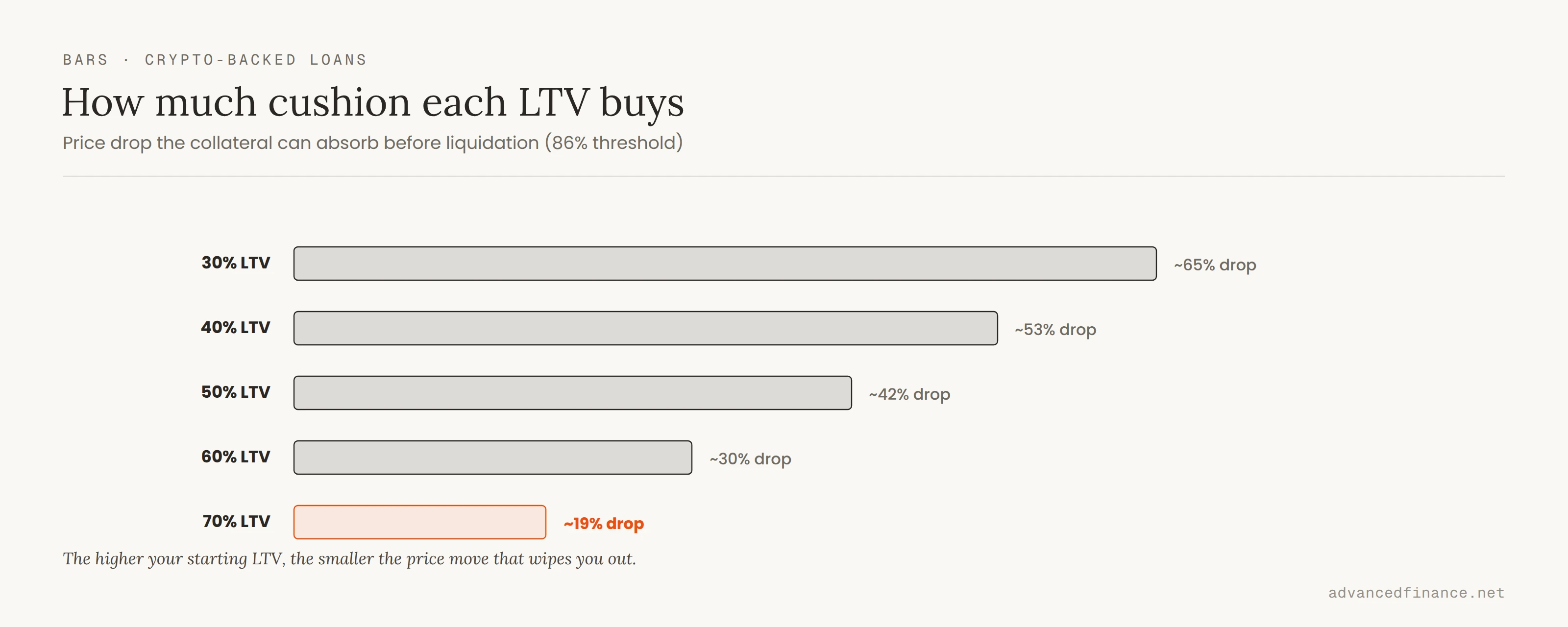

This also turns "start conservative" into a number. Holding the liquidation threshold at 86% and buying 1 BTC at an illustrative $100,000, here is how far the price can fall before liquidation at each opening LTV. The cushion depends only on your LTV and the threshold, not on your entry price:

| Opening LTV | Loan on 1 BTC | Liquidation price | Price drop before liquidation |

|---|---|---|---|

| 30% | $30,000 | ~$34,900 | ~65% |

| 40% | $40,000 | ~$46,500 | ~53% |

| 50% | $50,000 | ~$58,100 | ~42% |

| 60% | $60,000 | ~$69,800 | ~30% |

| 70% | $70,000 | ~$81,400 | ~19% |

At a 30% LTV the market has to fall by roughly two-thirds before you are touched; at 70% a routine correction does it. That single choice, made when you open the loan, matters more than any alert or top-up you set up afterward.

CeFi vs DeFi After 2022

Anyone writing about crypto loans before 2022 pointed you at Celsius and BlockFi. Both collapsed that year. Celsius froze withdrawals and filed for bankruptcy in July 2022; BlockFi followed in November after the FTX implosion and was later wound down entirely. Their failure was not a liquidation event — it was a custody and counterparty failure. Users could not reach their collateral because a company they trusted had lent it out and lost it. The same due diligence you would use to spot crypto scams and rug pulls applies to choosing a lender: if you do not hold the keys, you are trusting a balance sheet you cannot see.

The market that rebuilt after that looks different. The fastest-growing model is now onchain: in early 2025 Coinbase launched Bitcoin-backed loans routed through the DeFi protocol Morpho, later adding ETH-backed loans of up to $1 million, and the product surpassed $1 billion in originations. The loan is non-custodial and the liquidation rules live in a public smart contract rather than a private ledger. Pure DeFi lenders such as Aave and Compound never stopped operating through the entire 2022 cycle, precisely because they are overcollateralized and liquidate mechanically. The lesson traders took away is blunt: transparent, automated liquidation is uncomfortable, but opaque, discretionary custody is what actually wiped people out.

| CeFi (centralized) | DeFi (onchain) | |

|---|---|---|

| Who holds your collateral | A company (custodian) | A smart contract; you control the keys |

| Main failure mode | Counterparty / bankruptcy (Celsius, BlockFi) | Smart-contract bug or oracle failure |

| Liquidation | Company-run; policies vary | Automated, mechanical, unforgiving |

| Transparency | Private balance sheet | Public and verifiable onchain |

| Access | KYC; jurisdiction limits | Permissionless wallet, global |

Lenders, Rates and Costs

A snapshot of platforms operating in 2026. Terms move constantly, so treat this as a starting map and confirm current numbers on each platform before borrowing.

| Platform | Type | Collateral | Rate & terms |

|---|---|---|---|

| Coinbase | CeFi / DeFi (Morpho) | BTC, ETH | From ~4% APR; user-set LTV, liquidates near 86%; non-custodial onchain |

| Ledn | CeFi | BTC | ~11.5% APR (more with fees); from 50% LTV; Bitcoin-focused |

| Nexo | CeFi | BTC, ETH, stablecoins | 1.9%–18.9% APR; from 50% LTV; not available to US retail |

| Unchained | CeFi | BTC | From ~14% APR; min 50% LTV; collaborative custody |

| Arch Lending | CeFi | BTC / ETH / SOL | From ~8.5% APR; LTV 60% / 55% / 45% |

| Salt Lending | CeFi | BTC, ETH, stables | ~7.5%–10.5% APR; 30/50/70% tiers; 0% origination, 5% liquidation fee |

| Aave | DeFi | ETH, wBTC, stETH + | Variable market rate; ~80% liq. threshold (majors); overcollateralized |

| Compound | DeFi | ETH, wstETH + | Variable market rate; overcollateralized onchain |

What it actually costs. Rates in 2026 span a wide band — roughly the mid-single digits to the high teens in APR, depending on platform, collateral, loan size, and term. Onchain and Bitcoin-focused lenders tend to sit at the low end. Watch two costs beyond the headline rate. First, origination or setup fees: some lenders charge none (SALT lists a 0% origination fee), while others fold a fee into the effective rate (Ledn quotes roughly 11.5% APR but closer to 12.4% all-in). Second, and most overlooked, the liquidation penalty: if you are sold out, most platforms take an extra cut on top of your loss — SALT charges a 5% liquidation fee, and DeFi protocols pay whoever closes your position a "liquidation bonus" of a few percent, borne by you. A low headline rate on a lender that liquidates aggressively can cost far more than a higher rate on a gentler one.

Borrowing is only one way to get value from crypto you do not want to sell; earning yield through staking or yield farming is another, with a completely different risk profile. A loan gives you cash today at the cost of liquidation risk; staking gives you yield at the cost of lockups and protocol risk.

Staying Out of Liquidation

The entire discipline reduces to keeping distance between your LTV and the liquidation threshold. Concretely:

- Start conservative. An opening LTV of 50% or less on volatile collateral pushes your liquidation price far below the current market. The math above shows how much runway a smaller loan buys.

- Set price and margin alerts. Most CeFi platforms and onchain dashboards will warn you as your LTV or health factor deteriorates, giving you time to react before the threshold, not after.

- Keep dry powder to top up. Adding collateral or repaying part of the loan lowers your LTV instantly. That only helps if you have funds set aside and are watching — in a fast crash there may be no time to move money in.

- Consider stablecoin collateral. Backing a loan with stablecoins such as USDC removes almost all price-driven liquidation risk, at the cost of borrowing against an asset with little upside.

- Read the liquidation policy, not the rate. Grace periods, partial liquidations, and how quickly a platform sells vary widely. A slightly higher rate on a lender that liquidates gently can be cheaper than a "cheap" loan that dumps all your collateral at the first breach.

- Vet the lender itself. Beyond rates, check the custody model (do you hold the keys or does the company?), proof of reserves or audits, insurance, and jurisdiction. The 2022 failures were not market events — they were companies you could not see inside.

FAQ

How much do crypto-backed loans cost?

Expect an APR anywhere from the mid-single digits to the high teens in 2026, depending on platform, collateral, and loan-to-value — onchain and Bitcoin-focused lenders tend to be cheapest. Beyond interest, check for origination fees (some charge none) and, critically, the liquidation penalty: SALT, for example, adds a 5% fee if you are liquidated, and DeFi protocols pay a similar "liquidation bonus" to whoever closes your position.

Which assets can I use as collateral, and at what LTV?

Bitcoin and Ethereum are accepted almost everywhere; some platforms add Solana, other large tokens, or stablecoins. The more volatile the asset, the lower the LTV you will be offered — Bitcoin might start around 50% while a smaller altcoin is capped well below that. Stablecoin collateral carries the least liquidation risk but the least upside.

Are crypto-backed loans a taxable event?

Borrowing against your crypto is generally not a taxable event, because you have not sold anything — which is much of the appeal. However, a forced liquidation is a sale and can trigger capital gains. Rules vary by country, so confirm your situation with a tax professional.

Is it safer to borrow through CeFi or DeFi?

They fail in different ways. CeFi carries custody and counterparty risk — the Celsius and BlockFi lesson — because a company holds your assets. DeFi removes the custodian but adds smart-contract risk and unforgiving, automated liquidations. Onchain lending is transparent and non-custodial; centralized lending can be gentler but only as trustworthy as the company behind it.

What happens to my collateral if I get liquidated?

The lender sells just enough collateral to bring the loan back within its limit and usually adds a liquidation fee or bonus on top, so you keep the rest but crystallize a loss at a low price — often a taxable one. Liquidation is the outcome the whole exercise is meant to avoid.

Author's Insight

After years around crypto borrowers, the pattern is always the same: people are liquidated not because they were unlucky, but because they borrowed the maximum the platform allowed. Maxing your LTV feels efficient right up until a routine 20% dip becomes a forced sale. I treat the opening LTV as the single most important decision of the whole loan, and I size it for the drawdown I would find genuinely painful, not the one I expect. The platforms that collapsed in 2022 taught the other half of the lesson: know who holds your collateral. Between a transparent onchain liquidation I can see coming and an opaque custodian I have to trust, I will take the one I can watch every hour of the day.

Bottom Line

Crypto-backed loans unlock real liquidity without forcing a sale, but they hand the lender the right to sell for you if your LTV climbs into the liquidation zone. Your liquidation price is set by how much you borrow and the platform's threshold, so a conservative opening LTV, alerts, spare collateral, and a lender whose custody and liquidation policy you actually understand are what separate a useful loan from a forced loss. Borrow like the next crash starts tomorrow, and the math stays on your side.